How to Export Alcohol to the UK: Regulations, Duty, and Bonded Warehouse Process

Exporting alcohol to the UK involves more than arranging transport. Importers must navigate excise duty, VAT, HMRC registration requirements, and post-Brexit labelling rules before products can enter the retail supply chain.

This guide explains the full process — from establishing a compliant UK import structure to storing alcohol under bond and releasing it for domestic sale.

How UK Alcohol Taxation Works

Every shipment of spirits, wine, or beer entering the UK faces three potential charges:

- Excise duty — charged per unit of alcohol, based on product type and ABV

- Customs (import) duty — varies by country of origin and trade agreement status

- VAT — currently 20%, applied on top of duty-inclusive value

Under HMRC's duty suspension regime, these charges do not have to be paid at the point of import. Alcohol can be moved and stored in the UK under bond — with duty deferred until the goods are released into the domestic market.

Why this matters for cash flow: UK alcohol duty rates are among the highest in Europe. From August 2023, HMRC restructured the entire duty system — the biggest reform in 140 years — aligning rates by ABV rather than product category.

Spirits above 22% ABV attract £28.74 per litre of pure alcohol. Wine between 11.5% and 14.5% ABV now carries a flat rate of £2.67 per 75cl bottle (still wine). Holding these costs in suspension for weeks or months has material financial impact at scale.

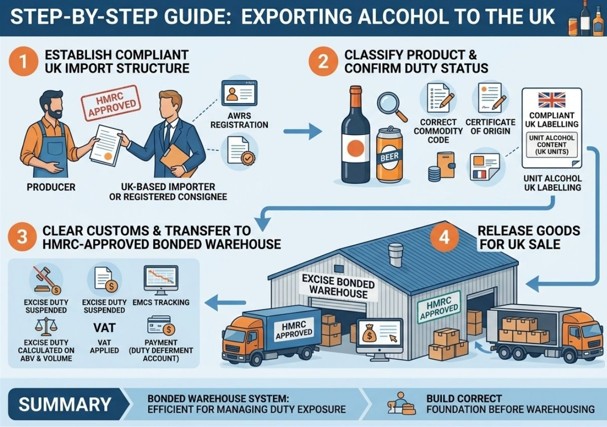

Step 1: Establish a Compliant UK Import Structure

Overseas producers cannot self-import under UK excise law. You need one of the following:

- A UK-based importer of record — a registered business responsible for the shipment, customs declarations, and duty liability

- A Registered Consignee — an HMRC-approved entity authorised to receive alcohol under duty suspension from overseas

- A fiscal representative or customs agent — used for documentation and import clearance but unable to hold duty liability independently

If your UK partner distributes to other businesses such as wholesalers or on-trade buyers, they must also be registered under the Alcohol Wholesaler Registration Scheme (AWRS). Selling to an unregistered wholesaler is a compliance breach that carries significant penalties.

Most new exporters enter the UK via an established importer-distributor that already holds the necessary HMRC approvals.

Step 2: Classify Your Product and Confirm Duty Status

Before customs clearance, shipments must be correctly classified and documented.

Key requirements include:

- The correct commodity code from the UK Global Tariff, which determines the import duty rate

- A certificate of origin when claiming preferential duty rates under trade agreements such as the UK–EU Trade and Cooperation Agreement (TCA)

- UK-compliant labelling including English-language labels, allergen declarations, and alcohol unit information

Northern Ireland operates under different rules due to the Windsor Framework. Goods entering Northern Ireland from the EU follow separate procedures compared with goods entering Great Britain, so exporters distributing across both markets must plan accordingly.

Step 3: Clear Customs and Transfer to an HMRC-Approved Bonded Warehouse

After customs clearance, alcohol can be transferred directly to an HMRC-approved bonded warehouse, also known as an Excise Warehouse.

Within this controlled environment:

- Excise duty remains suspended

- VAT is deferred

- Goods are monitored through the Excise Movement and Control System (EMCS), the UK's electronic system for tracking duty-suspended alcohol movements

Warehouse operators must hold HMRC approval as registered Warehouse Keepers. Not all logistics providers are authorised to operate under this regime.

From the warehouse, goods may be:

- Held for domestic sale

- Re-exported without triggering UK duty

- Consolidated or repackaged for specific orders

- Released gradually based on market demand

Step 4: Release Goods for UK Distribution

Excise duty and VAT become payable when alcohol leaves the bonded warehouse for sale within the UK.

At this stage:

- Excise duty is calculated using HMRC rate tables based on ABV and volume

- VAT is applied to the duty-inclusive value

- Approved importers can use a duty deferment account to pay duty monthly rather than per shipment

For large import operations, duty deferment significantly reduces administrative burden and improves cash-flow management.

Common Compliance Failures to Avoid

Several common mistakes can disrupt alcohol imports into the UK:

- Incorrect commodity codes, leading to incorrect duty calculations

- Non-compliant UK labelling, which can result in border detention or retailer rejection

- Using an unregistered AWRS wholesaler, placing the importer at legal risk

- Assuming EU compliance automatically applies in the UK, despite regulatory divergence after Brexit

Avoiding these issues is essential to maintaining a smooth supply chain.

Key Questions Exporters Often Ask

Do I need a UK entity to export alcohol to the UK?

Not necessarily. However, you must work with a UK-based importer or Registered Consignee approved by HMRC.

How long can alcohol be stored in a bonded warehouse?

There is no fixed statutory time limit. Goods can remain under duty suspension indefinitely as long as they stay within the authorised warehouse.

Does the UK–EU trade agreement eliminate alcohol import duty?

The agreement removes customs duty for qualifying goods with EU or UK origin. Excise duty still applies to all alcohol regardless of origin.

What changed in the 2023 UK alcohol duty reform?

HMRC introduced a unified ABV-based duty system replacing the previous category-based structure. This significantly altered duty costs for many wine and sparkling products.

Strategic Considerations for Alcohol Exporters

Entering the UK alcohol market requires more than a logistics provider. Exporters must coordinate importer registration, product classification, documentation, labelling compliance, and warehouse arrangements.

The bonded warehouse system is a central tool for managing duty exposure and maintaining supply chain flexibility. However, it only works effectively when the upstream structure — importer compliance, commodity codes, and regulatory documentation — is correctly established.

Building that foundation ensures alcohol can move through customs, bonded storage, and UK distribution without unnecessary delays or financial risk.

About the author: Purland House Ltd — specialists in HMRC bonded warehousing, customs compliance, and alcohol logistics in London.

Published on: 2026-03-11